Robust linear model estimation using RANSAC¶

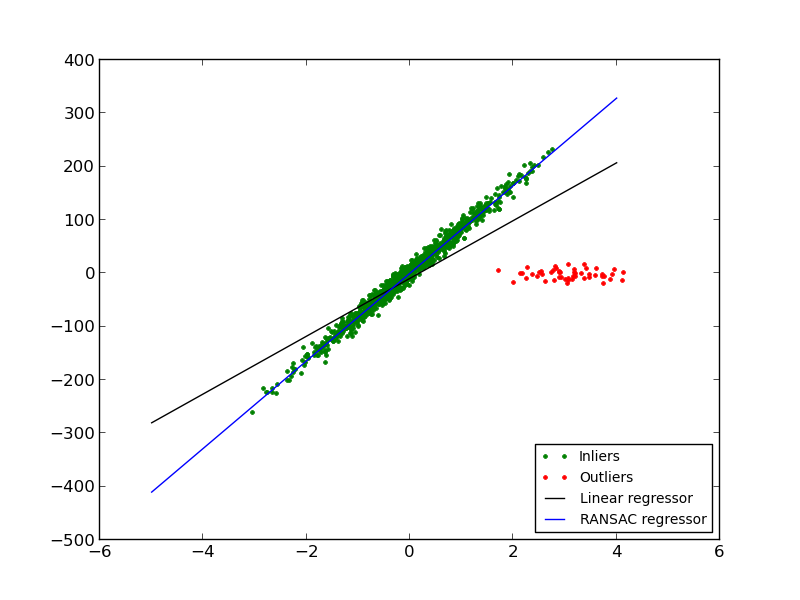

In this example we see how to robustly fit a linear model to faulty data using the RANSAC algorithm.

Script output:

Estimated coefficients (true, normal, RANSAC):

82.1903908408 [ 54.17236387] [[ 82.08533159]]

Python source code: plot_ransac.py

import numpy as np

from matplotlib import pyplot as plt

from sklearn import linear_model, datasets

n_samples = 1000

n_outliers = 50

X, y, coef = datasets.make_regression(n_samples=n_samples, n_features=1,

n_informative=1, noise=10,

coef=True, random_state=0)

# Add outlier data

np.random.seed(0)

X[:n_outliers] = 3 + 0.5 * np.random.normal(size=(n_outliers, 1))

y[:n_outliers] = -3 + 10 * np.random.normal(size=n_outliers)

# Fit line using all data

model = linear_model.LinearRegression()

model.fit(X, y)

# Robustly fit linear model with RANSAC algorithm

model_ransac = linear_model.RANSACRegressor(linear_model.LinearRegression())

model_ransac.fit(X, y)

inlier_mask = model_ransac.inlier_mask_

outlier_mask = np.logical_not(inlier_mask)

# Predict data of estimated models

line_X = np.arange(-5, 5)

line_y = model.predict(line_X[:, np.newaxis])

line_y_ransac = model_ransac.predict(line_X[:, np.newaxis])

# Compare estimated coefficients

print("Estimated coefficients (true, normal, RANSAC):")

print(coef, model.coef_, model_ransac.estimator_.coef_)

plt.plot(X[inlier_mask], y[inlier_mask], '.g', label='Inliers')

plt.plot(X[outlier_mask], y[outlier_mask], '.r', label='Outliers')

plt.plot(line_X, line_y, '-k', label='Linear regressor')

plt.plot(line_X, line_y_ransac, '-b', label='RANSAC regressor')

plt.legend(loc='lower right')

plt.show()

Total running time of the example: 0.13 seconds ( 0 minutes 0.13 seconds)